Forecasting day-ahead electricity prices: A review of state-of-the-art algorithms, best practices and an open-access benchmark

Abstract

While the field of electricity price forecasting has benefited from plenty of contributions in the last two decades, it arguably lacks a rigorous approach to evaluating new predictive algorithms. The latter are often compared using unique, not publicly available datasets and across too short and limited to one market test samples. The proposed new methods are rarely benchmarked against well established and well performing simpler models, the accuracy metrics are sometimes inadequate and testing the significance of differences in predictive performance is seldom conducted. Consequently, it is not clear which methods perform well nor what are the best practices when forecasting electricity prices. In this paper, we tackle these issues by comparing state-of-the-art statistical and deep learning methods across multiple years and markets, and by putting forward a set of best practices. In addition, we make available the considered datasets, forecasts of the state-of-the-art models, and a specifically designed python toolbox, so that new algorithms can be rigorously evaluated in future studies.

keywords:

Electricity price forecasting , Deep learning , Open-access benchmark , Forecast evaluation , Best practices for price forecasting1 Introduction

The increasing penetration of renewable energy sources (RES) in today’s power systems makes electricity generation more volatile and the resulting electricity prices harder to predict [1, 2, 3, 4]. On the other hand, advances in electricity price forecasting (EPF) constantly provide new tools with the ultimate objective of narrowing the gap between predictions and actual prices. The progress in this field, however, is not steady and easy to follow. In particular, as concluded by all major review publications, comparisons between EPF methods are very difficult since studies use different datasets, different software implementations, and different error measures; the lack of statistical rigor complicates these analyses even further [5, 6, 7, 8]. In particular:

-

1.

There are several studies comparing machine learning (ML) and statistical methods but the conclusions of these studies are contradictory. Typically, studies considering advanced statistical techniques only compare them with simple ML methods [9, 10, 11] and show that statistical methods are obviously better. Conversely, studies proposing new ML methods only compare them with simple statistical methods [12, 13, 14, 15, 16] and show that ML models are more accurate.

-

2.

In many of the existing studies [17, 18, 19, 20, 21, 22, 23] the testing periods are usually too short to yield conclusive results. In some cases, the test datasets are limited to one-week periods [24, 25, 22, 26, 27, 28, 29, 30]; this ignores the problem of special days, e.g. holidays, and is not representative for the performance of the proposed algorithms across a whole year. As argued in [5], to have meaningful conclusions, the test dataset should span at least a year.

-

3.

Some of the existing papers do not provide enough details to reproduce the research. The three most common issues are: (i) not specifying the exact split between the training and test dataset [31, 32, 33, 34, 35, 36, 37], (ii) not indicating the inputs used for the prediction model [38, 35, 39, 40, 36], and (iii) not specifying the dataset employed [41, 42, 21, 33]. This obviously prevents other researchers from validating the research results.

These three problems have aggravated over the last years with the increase in popularity of deep learning (DL). While new published papers on DL for EPF appear almost every month, and most claim to develop models that obtain state-of-the-art accuracy, the comparisons performed in those papers are very limited. Particularly, the new DL methods are usually compared with simpler ML methods [43, 44, 30, 28, 45, 46, 47]. This is obviously problematic as such comparisons are not fair. Moreover, as the proposed methods are not compared with other DL algorithms, new DL methods are continuously being proposed but it is unclear how the different models perform relatively to each other.

Similar problems arise in the context of hybrid methods. In recent years, very complex hybrid methods have been proposed. Typically, these hybrid models are based on combining a decomposition technique, a feature selection method, an ML regression model, and sometimes a type of genetic algorithm for optimization purposes. As with DL algorithms, these studies usually avoid comparisons with well-established methods [42, 21, 48, 49, 34, 25, 50] or resort to comparisons using outdated methodologies [26, 51, 52, 22, 41, 24, 37]. In addition, while a specific genetic algorithm or decomposition technique is considered, most of the studies do not analyze the effect of selecting a variant of these techniques [24, 21, 50, 51, 52]. Thus, the relative importance of each of the different components of the hybrid methods it is not even clear.

1.1 Motivation and contributions

The above mentioned problems call for three actions.

Firstly, implementing in a popular programming environment (e.g. python), thoroughly testing and making available a set of simple but powerful open-source forecasting methods, which can potentially obtain state-of-the-art results, and that researchers can easily use to evaluate any new forecasting model.

Secondly, collecting and making freely available to the EPF community a set of representative benchmark datasets that researchers can use to evaluate and compare their methods using long testing periods. Although, some datasets are available for download without restrictions, e.g. as supplements to published articles [53] or sample transaction data [54], they are typically limited in scope (one market, a 2-3 year timespan or price series only). Hence, conclusions from such datasets are limited, results can hardly be extrapolated to other markets, and the relevance of the studies using such data are not entirely clear.

Thirdly, putting forward a set of best practices so that the conclusions of EPF studies become more meaningful and fair comparisons can be made.

In this paper, we try to tackle the above via three distinct contributions:

-

1.

We analyze the existing literature and select what could arguably be considered as state-of-the-art among statistical and machine learning methods: the Lasso Estimated AutoRegressive (LEAR) model111Originally introduced in [55] under the name LassoX and based on the fARX model, a parameter-rich autoregressive specification with exogenous variables. The name refers to the least absolute shrinkage and selection operator (LASSO) [56] used to jointly select features and estimate their parameters. Very similar models were used in [57] under the name 24lassoDoW,nl and in [58] under the name 24Lasso. [55] and the Deep Neural Network (DNN) [59], a relatively simple and automated DL method that optimizes hyperparameters and features using Bayesian optimization. Then, we make our models open-source and available to other researchers as part of an open-source python library https://github.com/jeslago/epftoolbox specially designed for this study to provide a common research framework for EPF research [60]. Besides the models, we also provide extensive documentation [61] for the library.

-

2.

We propose a set of five open-access benchmark datasets spanning six years each, that represent a range of well-established day-ahead, auction type power markets from around the globe. The datasets contain day-ahead electricity prices at an hourly frequency and two relevant exogenous variables each. They can be accessed from the mentioned python library [60] that is specially designed for this study. Together with the datasets, the library also includes the forecasts of the open-access methods across the five benchmark datasets so that researchers can quickly make further comparisons without having to re-train or re-estimate the models.

-

3.

We provide a set of best practice guidelines to conduct research in EPF so that new studies are more sound, reproducible, and the obtained conclusions are stronger. In addition, we include some of the guidelines, e.g. adequate evaluation metrics or statistical tests, in the the mentioned python library [60] that is specially designed for this study to provide a common research framework for EPF research

1.2 Paper structure

The remainder of the paper is organized a follows. Section 2 performs a literature review of the current state of EPF. Sections 3 and 4 respectively present the open-access benchmark datasets and the open-source benchmark models. Section 5 describes the set of guidelines and best practices when performing research in EPF. Section 6 discusses the forecasting results for all five datasets. Finally, Section 7 provides a summary and a checklist of the requirements for meaningful EPF research.

2 Literature review

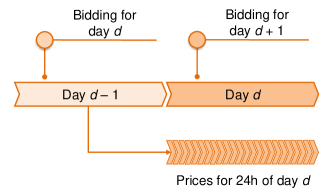

The field of EPF aims at predicting the spot and forward prices in wholesale markets, either in a point or probabilistic setting. However, given the diversity of trading regulations available across the globe, EPF always has to be tailored to the specific market. For instance, the workhorse of European short-term power trading is the day-ahead market with its once-per-day uniform-price auction, see Fig. 1. On the other hand, the Australian National Electricity Market operates as a real-time power pool, where a dispatch price is determined every five minutes and six dispatch prices are averaged every half hour as pool prices [62], while electricity forward markets share many aspects with those of other energy commodities (oil, gas, coal), and quite often are only financially settled [63].

As the field of EPF is very diverse, a complete literature review is out of the scope of this paper. Instead, this section is intended to provide an overview of the the three families of methods, i.e. statistical, ML, and hybrid methods, proposed for point forecasting in day-ahead markets since 2014, i.e. since the last comprehensive literature review of Weron [5]. The more recent reviews either focused on short-terk [6] and medium-/long-term [7] probabilistic EPF, were not that comprehensive in scope [64, 65], or concerned electricity derivatives [63]. Furthermore, our survey puts a special emphasis on DL and hybrid methods as this is the area of EPF characterized by the most rapid development and, at the same time, troubled by non-rigorous empirical studies which motivated us to write this paper in the first place.

2.1 Statistical methods

Most models in this class rely on linear regression and represent the dependent (or output) variable, i.e. the price for day and hour , by a linear combination of independent (or predictor, explanatory) variables, also called regressors, inputs, or features:

| (1) |

where is a row vector of coefficients specific to hour , is a column vector of inputs and is an error term; the intercept can be set to zero if the data is demeaned beforehand. Note that here we are using a notation common in day-ahead forecasting, which emphasizes the vector structure of these price series, see Fig. 1. Alternatively we could use single indexing: with . Although the multivariate modeling framework has been shown to be marginally more accurate than the univariate counterpart, both approaches have their pros and cons [57, 66].

In the last few years, there have been several key contributions in the field of statistical methods for EPF. Arguably, the most relevant of them has been the appearance of linear regression models with a large number of input features that utilize regularization techniques [56, 67]. Classically, the regression model in (1) is estimated using ordinary least squares (OLS) by minimizing the residual sum of squares (RSS), i.e. squared differences between the predicted and actual values. However, if the number of regressors is large, using the least absolute shrinkage and selection operator (LASSO) [56] or its generalization the elastic net [67] as implicit feature selection methods have been shown to improved the forecating results [68, 55, 69, 57, 58, 59]. In particular, by jointly minimizing the RSS and a penalty factor of the model parameters (see Section 4.2 for details), these two implicit regularization techniques set some of the parameters to zero and thus effectively eliminate redundant regressors. As shown in the cited studies [68, 55, 69, 57, 58, 59], these parameter-rich222We define a parameter-rich linear model as a model with multiple regressors. regularized regression models exhibit superior performance. It is important to note that such an approach, called here Lasso Estimated AutoRegressive (LEAR), is in fact hybrid since LASSO (and electic nets) are considered ML techniques by some authors. However, we classify it as statistical because the underlying model is autoregressive.

Aside from proposing parameter-rich models and advanced estimators, researchers have also improved the field by considering a variety of additional preprocessing techniques. Most notably, models using so-called variance stabilizing transformations [70, 71, 9, 57] and long-term seasonal components [72, 73, 74, 75] have been proposed and shown to result in statistically significant improvements. However, the applicability of these two techniques varies greatly: due to very common occurrence of price spikes, variance stabilizing transformations have become a standard and replaced the commonly used logarithmic transformation (no longer applicable due to zeros and negative values333The logarithmic of 0 or a negative value is undefined.) to normalize electricity prices. By contrast, the applicability of long-term seasonal components has been more limited and it is unknown whether their beneficial effect is limited to relatively parsimonious regression models or also holds for parameter-rich models.

A third innovation in the field is an ensemble, i.e. a method that combines individual forecasting models to enhance the accuracy, that combines multiple forecasts of the same model calibrated on different windows. In this context, two different studies [76, 77] showed that the best results are obtained with a combination of a few short (spanning 1-4 months) and a few long calibration windows (of approximately two years). Said ensembles were able to significantly outperform predictions obtained for the best ex-post selected calibration window [76, 77]. But again, it has not been shown to date whether this effect is limited to relatively parsimonious regression models or also holds for LEAR models.

2.2 Deep learning

In the last five years, a total of 28 deep learning papers in the context of EPF have been published444This data is based on two searches in Scopus looking for keywords in the title, abstract, and keywords. The first search is based on the following query TITLE-ABS-KEY(((("forecasting electricity") OR ("predicting electricity")) AND (("electricity spot") OR ("electricity day-ahead") OR ("electricity price"))) OR ((("price forecasting") OR ("price prediction") OR ("forecasting price") OR ("predicting price") OR ("forecasting spikes") OR ("forecasting VAR")) AND (("electricity spot price") OR ("electricity price") OR ("electricity market") OR ("day-ahead market") OR ("power market"))) AND ("deep") AND ("learning")). The second search is very similar but replacing ("deep") AND ("learning") by ("neural") AND ("network").. Moreover, this number has been steadily increasing: while in 2016 there was only one paper and in 2017 none, in 2018 there were 11, and in 2019 there were 16. Despite this trend, most of the published studies are very limited: the comparisons are too simplistic, e.g. avoid state-of-the-art statistical methods, and their results cannot be generalized.

The first published DL paper [12] proposes a deep learning network using stacked denoising autoencoders. The paper, despite being the first, provides a better evaluation than most studies: the new method is compared not only against machine learning techniques but also against two statistical methods. Yet, the evaluation is limited as it is done considering three months of test data and employing simple models for comparison. In the second published DL paper [43], a DNN for modeling market integration is proposed. While the method is evaluated over a year of data, the study is also limited as the proposed model is not compared against other machine learning or statistical methods.

In the third published paper [59], four DL models (a DNNs, two recurrent neural networks (RNNs), and a convolutional network (CNN)) are proposed. This study is, to the best of our knowledge, the most complete study up to date. In particular, the proposed DL models are compared using a whole year of data against a benchmark of 23 different models, including 7 machine learning models, 15 statistical methods, a commercial software. Moreover, among the statistical methods, the comparison includes the fARX-Lasso and fARX-EN, i.e. the state-of-the-art statistical methods. While the study shows the superiority of the DL algorithms, very strong conclusions are not possible as the study only considers a single market.

The studies that followed in 2018 focused on one of three topics: 1) evaluating the performance of different deep recurrent networks [13, 23, 78, 37]; 2) proposing new hybrid methods based on CNNs and LSTMs [44, 14, 79, 80]; or 3) employing regular DNN models [23]. Independently of the focus, they were all more limited than the first and the third studies [12, 59] as they failed to compare the new DL models with state-of-the-art statistical methods and/or to employ long enough datasets to derive strong conclusions.

In detail, [13] studies the use of RNNs for forecasting electricity prices but the comparison is done in a single market and against simple statistical methods (a seasonal auto regressive integrated moving average (ARIMA) model, a Markov regime-switching model, and a self exciting threshold model). Moreover, while the comparison includes other DL methods, it avoids comparison with simpler ML techniques. Ref. [44] proposes a hybrid DL methods composed of a CNN and a long short-term memory (LSTM) (a type of recurrent network) for forecasting balancing prices. However, the new model is only compared against simple ML benchmarks and the evaluation is done using different periods comprising three months for training and 1 month for testing. Similarly, [14] proposes another hybrid model combining a CNN and an LSTM, but the model is only compared against two naive statistical methods: an auto regressive moving average (ARMA) and a generalized autoregressive conditional heteroskedasticity (GARCH) model.

In [23] a regular DNN model is proposed but the model is only evaluated on a test dataset comprising a single day and compared against a simple MLP. In [29], the use of an LSTM model for EPF is evaluated, but the method is only compared with three neural networks and a simple statistical method, and the evaluation is done using only 4 weeks of data. Likewise, [78] proposes a model based on an LSTM but a comparison against other methods is not done and the test dataset only comprises 2 weeks of data. In [37], another LSTM model is proposed but, as other studies, the test dataset comprises some months of data and the method is only compared against a simple decision tree and a support vector regressor; moreover, the exact split between the training and test dataset is not specified and it is unclear what is exactly the performance of the model. An exception to these studies is [81] which proposes a series of DL models and compares them for a year of data against several advanced statistical methods such as LASSO and a simpler ML method. The main drawbacks of the study are that it is based on a single market and that it only considers a simple ML method as a benchmark. In addition, the study focuses on intraday electricity prices, while most of the literature (including the current paper) considers forecasting day-ahead electricity prices.

In 2019, the main focus of the papers was the same as in 2018: 1) evaluating the performance of different deep recurrent networks (mostly LSTMs) [30, 45, 16, 47, 82, 83, 84], 2) proposing new hybrid deep learning methods usually based on LSTMs and CNNs [85, 86, 82, 87, 28, 17, 36], or 3) employing regular DNN models [46, 15, 88]. Similarly, as with most studies in 2018, the new studies were more limited than [12, 59] as no comparisons with state-of-the-art statistical methods were made and long test datasets were seldom used. In this context, even though some studies [16, 88] tried to compare the proposed methods with existing DL models [59], they either failed to re-estimated the benchmark models for the new case study [16] or they overfitted the DL benchmark models [88].

In detail, [30] proposes different LSTM models but the new models are only compared against 5 other ML techniques and using a test period of 4 weeks. In [28], a CNN model is proposed but the new model is just compared against three simple ML methods and using a test dataset that comprises a week. In [45], a model based on an LSTM is proposed but it is only compared against three simple ML methods and for a period of 12 weeks. In [46], the performance of a DNN is compared to that of an SVR model and, as the comparison only includes these two models, it is obviously very limited. In [15], a DNN is used as part of a two-step forecasting method; as in many other studies, the comparison is performed for one month of data and limited to two simple ML models (a SVR and an MLP) and a standard linear model. In [47], two DL models are proposed but the models are only compared to very simple ML methods (extreme learning machines and standard MLPs) and using a test dataset spanning eight months. In [16], a bidirectional LSTM to forecast prices in the French market is proposed; however, the study only considers historical prices as input features and the proposed method is only compared against DL models and a simple autoregressive model. In addition, the benchmark DL models are copied from [59] (a completely different case study that considers exogenous inputs and a different market) without re-tuning the hyperparameters to the new case study.

In [88], a neural network that uses data from order books is proposed and compared against DL methods from the literature, e.g. the ones proposed in [59]. While the new model outperforms existing DL methods, the DL methods from the literature are trained to overfit the training dataset555In the training dataset, the proposed model and some naive ML benchmark models yield a root mean square error in the order of 6. For the test dataset, for the same models, that error is between 9 and 12. By contrast, the training error of the benchmark DL model is 2, and the test error is 20. Having a training error that is 1/3 of the error of other models but a test error that is 10 times larger than the training error is a clear sign for overfitting (especially when for the rest of the models the test error is just 1.5 larger than the training error).. Therefore, the comparison is not meaningful (the DL benchmark models will necessarily perform poorly in the test dataset) and it cannot be assessed how the new model performs. In [85], a hybrid DL forecasting method is proposed based on stacked denoising autoencoders for pre-training, regular autoencodes for feature selection, and a rough DNN as a forecasting method. As other studies, the method is only compared against other simpler ML models. Moreover, the importance of each of the four modules of the hybrid method is not studied and the study does not re-calibrate the models with new data: the models are trained once and evaluated during a whole year. Similarly, [86] proposes a CNN hybrid model that uses mutual information, random forests, grey correlation analysis, and recursive feature elimination for feature selection. Unlike most models, the algorithm is trained to classify prices instead of predicting their scalar values; however, details of how this process is done are not provided. In addition, the method is only compared against simpler ML methods and evaluated for less than a year of data (the study uses 1 year for testing and training but the split is not specified). Likewise, [36] proposes a hybrid model based on CNNs and RNNs in the context of microgrids; as other studies, the method is evaluated in a small dataset, it is not compared against state-of-the-art statistical methods, and the exact split between training and test datasets is not specified.

2.3 Hybrid methods

Within the field of EPF, the research area that has received most attention in the last 5 years has been hybrid forecasting methods. In this time frame, more than 100 articles proposing new hybrid methods have been published666This data is based on two searches in Scopus looking for keywords in the title, abstract, and keywords. The first search is based on the following query TITLE-ABS-KEY(((forecast*) OR (predict*)) AND (electricity) AND (price*) AND (hybrid)). The second search is very similar but replacing the keyword hybrid by neural AND network. Note that, while this search is not as complete as the one for DL, it provides enough material for building an overview of the state of the field., i.e. approximately 5 times more than articles based on DL. Hybrid models are very complex forecasting frameworks that are composed of several algorithms. Usually, they comprise at least two of the following five modules:

-

1.

An algorithm for decomposing data.

-

2.

An algorithm for feature selection.

-

3.

An algorithm to cluster data.

-

4.

One or more forecasting models whose predictions are combined.

-

5.

Some type of heuristic optimization algorithm to either estimate the models or their hyperparameters.

In terms of decomposition methods, the most widely used technique is the wavelet transform [17, 19, 51, 52, 41, 49, 34, 22, 24, 89]. Alternatives methods include empirical mode decomposition [90, 32], variational mode decomposition [27, 48], and singular spectrum analysis [91, 92].

For feature selection, the most commonly used algorithms are correlation analysis [41, 42, 93, 94, 32] and the mutual information technique [95, 18, 52, 42, 96, 97]. Other algorithms include classification and regression trees with recursive feature elimination [50] or Relief-F [50].

For clustering data, the algorithms are usually based on one of the following four: k-means [26, 98], self-organizing maps [19, 26, 99], enhanced game theoretic clustering [26], or fuzzy clustering [100, 52]

The selection of forecasting models is much more diverse. The most widely used method is the standard MLP [19, 51, 41, 42, 91, 92, 96, 94, 32, 20, 97], followed by the adaptive network-based fuzzy inference system (ANFIS) [90, 95, 19], radial basis function network [100, 24, 20], and autoregressive models like ARMA or ARIMA [90, 22, 24, 20]. Other models include LSTM [17], linear regression [50], extreme learning machine [50, 22], CNN [50], Bayesian neural network [26, 99], exponential GARCH [90], echo state neural network [27], Elman neural networks [18], and support vector regressors [20]. It is important to note that in many of the approaches, the hybrid method does not consider a single forecasting model but combines several of them [50, 90, 20, 24, 19, 97].

Just as for the forecasting model, the diversity of the heuristic optimization algorithms is also large. While the most often utilized algorithm is particle swarm optimization [95, 51, 100, 48, 96, 22], many other approaches are also used: differential evolution [27], genetic algorithm [95], backtracking search [95], deterministic annealing [100], bat algorithm [41], vaporization precipitation-based water cycle algorithm [93], cuckoo search [92, 94], or honey bee mating optimization [24].

In spite of the large number of published works, the research in hybrid methods suffers from the same problems as discussed earlier. First, most of the studies either avoid comparison with well-established methods [42, 21, 48, 49, 34, 25, 50, 90, 27, 95, 18, 19, 100, 20, 93] or resort to comparisons using outdated methodologies [26, 51, 52, 22, 41, 24, 91, 92]. Hence, the accuracy of the new proposed methods cannot be accurately established.

Second, the considered studies usually employ very small datasets consisting either of a few days [17, 18, 19, 20, 21, 22] or a few weeks [24, 25, 22, 26, 27, 95, 18, 19, 93, 49, 41, 51, 100, 42, 91, 92]. Thus, drawing conclusions is nearly impossible and it is unclear whether the accuracy results are just the outcome of selecting a convenient test period.

Besides these two problems, for many hybrid methods the effect of selecting variants of the different hybrid components is not analyzed [24, 21, 50, 51, 52, 27, 20, 41, 42, 91, 92, 25]. Thus, it is not clear how relevant or useful the individual components are.

2.4 State-of-the-art models

Because of the described problems when comparing EPF models, it is very hard to establish what are the state-of-the-art methods. Nevertheless, considering the studies performed in the last years, it can be argued that the LEAR is a very accurate (if not the most accurate) linear model. Moreover, it can also be argued that the accuracy of this model can be further improved by transforming the prices using variance stabilizing transformations, combining forecasts obtained for different calibration windows, and/or using long-term seasonal decomposition.

For the case of ML models, the selection is harder as the existing comparisons are of worse quality. Considering the most complete benchmark study in terms of forecasting models [59], it seems that a simple DNN with two layers is one of the best ML models. In particular, while more complex models, e.g. LSTMs, could potentially be more accurate, there is at the moment no sound evidence to validate this claim.

In the case of hybrid models, establishing what is the best model is an impossible task. Firstly, while many hybrid methods have been proposed, they have not been compared with each other nor with the LEAR or DNN models. Secondly, as most studies do not evaluate the individual influence of each hybrid component, it is also impossible to establish the best algorithms for each hybrid component, e.g. it is unclear what are the best clustering, feature selection method, or data decomposition methods.

With that in mind, we will consider the LEAR and the DNN for the proposed open-access benchmark. In particular, not only are these two methods highly accurate, but they are also relatively simple. As such, we think that they are the best benchmarks to compare new complex EPF forecasting methods with.

3 Open-access benchmark dataset

The first contribution of the paper is to provide a large open-access benchmark dataset on which new methods can be tested, together with the day-ahead forecasts of the proposed open-access methods. In this section, we introduce this dataset, which can be accessed777Note that we do not own the data in the dataset. However, it can be freely accessed from different websites, e.g. the ENTSO-E transparency platform [101]. In this context, the proposed python library [60, 61] provides an interface to easily access the data. using the python library built for this study.

3.1 General characteristics

For a benchmark dataset in EPF to be fair it should satisfy three conditions: 1) comprise several electricity markets so that the capabilities of new models can be tested under different conditions, 2) be long enough so that algorithms can be analyzed using out-of-sample datasets that span 1-2 years, and 3) be recent enough to include price effects due to the integration of RES.

Based on these conditions, we propose five datasets representing five different day-ahead electricity markets, each of them comprising 6 years of data. The prices of each market have very distinct dynamics, i.e. they all have differences in terms of the frequency and existence of negative prices, zeros prices, and price spikes. In addition, as electricity prices depend on exogenous variables, each dataset comprises two additional time series: day-ahead forecasts of two influential exogenous factors that differ from each market. The length of each dataset equals 2184 days, which translates to six years of 364 days or weeks888Electricity prices have weekly seasonality. Thus, by approximating a year by 52 weeks because we ensure that the metrics are not offset because a certain day, e.g. Monday, is harder to predict than the others.. All available time series are saved using the local time, and the daylight savings are treated by either arithmetically averaging two values from the extra hour or interpolating the neighboring values for the missing observation.

3.2 Nord Pool

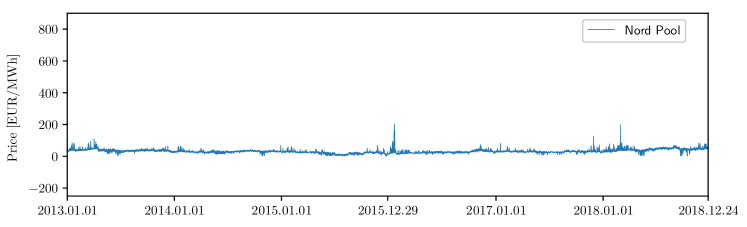

The first dataset represents the Nord Pool (NP), i.e. the European power market of the Nordic countries, and spans from 01.01.2013 to 24.12.2018. The dataset contains hourly observations of day-ahead prices, the day-ahead load forecast, and the day-ahead wind generation forecast. The dataset was constructed using the data freely available on the webpage of the Nordic power exchange Nord Pool [54]. Figure 2 (top) displays the electricity price time series of the dataset; as can be seen, the prices are always positives, zero prices are rare, and prices spikes seldom occur.

3.3 PJM

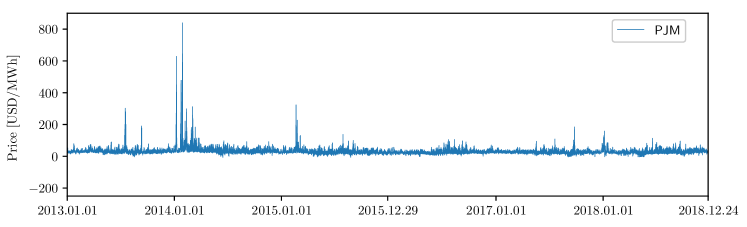

The second dataset is obtained from the Pennsylvania-New Jersey-Maryland (PJM) market in the United States. It covers the same data points as Nord Pool, i.e. from 01.01.2013 to 24.12.2018. The three time series are: the zonal prices in the Commonwealth Edison (COMED) (a zone located in the state of Illinois) and two day-ahead load forecast series, one describing the system load and the second one the COMED zonal load. The data is freely available on the PJM’s website [102]. Figure 2 (bottom) represents the electricity price time series of the dataset; as with the NP market, the prices are always positive and zero prices are rare; however, unlike with the prices in the NP market, spikes appear frequently.

3.4 EPEX-BE

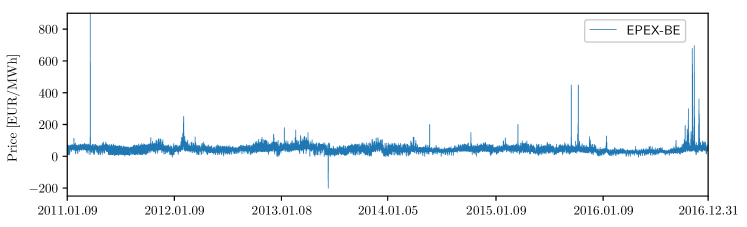

The third dataset represents the EPEX-BE market, the day-ahead electricity market in Belgium, which is operated by EPEX SPOT. The dataset spans from 09.01.2011 to 31.12.2016. The two exogenous data series represent the day-ahead load forecast and the day-ahead generation forecast in France. While this selection might be surprising, it has been shown [43] that these two are the best predictors of Belgian prices. The price data is freely available in the ENTSO-E transparency platform [101] and the ELIA website [103], and the load and generation day-ahead forecasts are freely available in [104]. It is important to note that this dataset is particularly interesting because it is harder to predict. Figure 3 (top) shows the electricity price time series of the dataset; unlike the prices in the PJM and NP markets, negative prices and zero prices appear more frequently, and price spikes are very common.

3.5 EPEX-FR

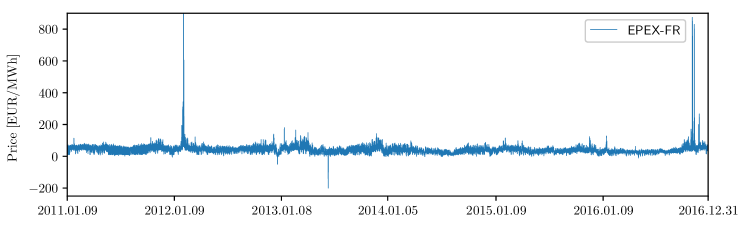

The fourth dataset represents the EPEX-FR market, the day-ahead electricity market in France, which is also operated by EPEX SPOT. The dataset spans the same period as the EPEX-BE dataset, i.e. from 09.01.2011 to 31.12.2016. Besides the electricity prices, the dataset comprises the day-ahead load forecast and the day-ahead generation forecast. As before, the price data is freely obtained from the ENTSO-E transparency platform [101], and the load and generation day-ahead forecasts are freely available on the webpage of RTE [104], i.e. the transmission system operator (TSO) in France. Figure 3 (middle) displays the electricity price time series of the dataset; as in the EPEX-BE market, negative prices, zero prices, and spikes are very common.

3.6 EPEX-DE

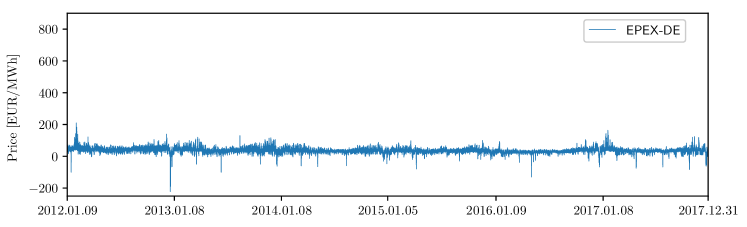

The last dataset describes the EPEX-DE market, the German electricity market, which is also operated by EPEX SPOT. The dataset spans from 09.01.2012 to 31.12.2017. Besides the prices, the dataset comprises the day-ahead zonal load forecast in the TSO Amprion zone and the aggregated day-ahead wind and solar generation forecasts in the zones of the 3 largest999There are 4 TSOs in Germany. TSOs (Amprion, TenneT, and 50Hertz). The price data is freely obtained from the ENTSO-E transparency platform [101], the zonal load day-ahead forecasts is freely available in the website of Amprion [105], and the wind and solar forecasts in the websites of Amprion [105], 50Hertz [106], and TenneT [107]. Figure 3 (bottom) displays the electricity price time series of the dataset; as can be seen, while negative and zero prices occur more often than in the other four markets, price spikes are more rare.

3.7 Training and testing periods

For each dataset, the testing period is defined as the last 104 weeks, i.e. the last two years, of the dataset. The exact dates of the testing datasets are defined in Table 1.

| Market | Test period |

|---|---|

| Nord pool | 27.12.2016 – 24.12.2018 |

| PJM | 27.12.2016 – 24.12.2018 |

| EPEX-FR | 04.01.2015 – 31.12.2016 |

| EPEX-BE | 04.01.2015 – 31.12.2016 |

| EPEX-DE | 04.01.2016 – 31.12.2017 |

It is important to note that, as we will argue in Section 5, selecting two years as the testing period is paramount to ensure good research practices in EPF.

Unlike the testing dataset, the training dataset cannot be defined as it will vary between different models. In, general, the training dataset will comprise any data that is prior to the data under study. However, the exact data will change depending on two concepts, i.e. calibration window and recalibration:

-

1.

While there are four years of data available for estimating the model, it might be desirable to employ only recent data, e.g. to avoid estimating effects that no longer play a role. The amount of past data employed for estimation defines the calibration window.

-

2.

The model can be estimated once and then evaluated for the full test dataset, or it can be continuously recalibrated on daily basis to incorporate the input of recent data.

For example, let us consider predicting the prices in the NP on 15.02.2017. A model using a calibration window of 52 weeks and no recalibration would employ a training dataset comprising the data between 29.12.2016 and 26.12.2016, i.e. one year prior to the start of the test period. By contrast, a model using a calibration window of 104 weeks and daily recalibration would employ the data between 18.02.2015 and 14.02.2017.

4 Open-access benchmark models

The second contribution of the paper is to provide a set of state-of-the-art open-source forecasting methods as an open-source python toolbox. As explained in Section 2.4, the LEAR [55] and the DNN [59] models are not only highly accurate but also relatively simple. Therefore, we implement these two methods and provide their code freely available as part of the proposed toolbox [60, 61]. It is important to note that the use of the proposed open-access methods is fully documented and automated so researchers can test and use them without expert knowledge.

For the sake of simplicity, the description provided here is limited to the bare minimum. For further details on the two models we refer to the original papers [55, 59].

4.1 Input features

Before describing each model, let us define the input features that are considered. Independently of the model, the available input features to forecast the 24 day-ahead prices of day , i.e. , are the same:

-

1.

Historical day-ahead prices of the previous three days and one week ago, i.e. , , , .

-

2.

The day-ahead forecasts of the two variables of interest (see Section 3 for details) for day available on day , i.e. and ; note that the variables of interest are different for each market.

-

3.

Historical day-ahead forecasts of the variables of interest the previous day and one week ago, i.e. , , , .

-

4.

A dummy variable that represents the day of the week. In the case of the linear model, following the standard practice in the literature [58, 55, 77], this is a binary vector that encodes every day of the week by setting all elements to zero except the element that identifies the day of the week, e.g. represents Monday and Tuesday. In the case of the neural network, for the sake of simplicity, the day of the week is modeled with a multi-value input .

In total, we consider a total of 247 available input features for each LEAR model and 241 input features for each DNN model. It is important to note that, while the available input features are the same, each method performs a different feature selection procedure:

-

1.

Each of the LEAR models finds the optimal set of features using LASSO as an embedded feature selection, i.e. each of the models uses L1-regularization to select among the 247 features.

-

2.

For the DNN, as in the original study [59], the input features are optimized together with the hyperparameters using the tree Parzen estimator [108] (see Section 4.3 for details).

In both cases, the feature selection is fully automated and does not require expert intervention.

4.2 The LEAR model

The first model is the LEAR model [55], a parameter-rich ARX model estimated using LASSO as an implicit feature selection approach. To enhance the model as shown by [9], the data is preprocessed with the arc hyperbolic sine (asinh) variance stabilizing transformation. Long-term seasonal decomposition is not considered for the sake of simplicity; particularly, while it has been shown to further improve the performance of the LEAR, we leave it out for future research.

As in [77], to further enhance the model, we recalibrated daily over different calibration window lengths: 8 weeks, 12 weeks, 3 years, and 4 years. We consider short windows (8-12 weeks) in combination with long windows (3-4 years) because it has been empirically shown to lead to better results [77]. In this context, we consider a minimum of 8 weeks as lower windows might not have enough information to correctly estimate parameter-rich models [77].

The LEAR model to predict price on day and hour is defined by:

| (2) | ||||||

where are the 247 parameters of the LEAR model for hour . Many of these parameters become zero when (2) is estimated using LASSO:

| (3) |

where is the sum of squares residuals, the price forecast, is the number of days in the training dataset, and is the tuning (or regularization) hyperparameter of LASSO. Due to the computational speed of estimating with LASSO, during every daily recalibration, the hyperparameter that regulates the L1 penalty is optimized. This can be done using an ex-ante cross-validation procedure [109]. In this study, to further reduce the computational cost, we propose an efficient hybrid approach to perform the optimal selection of . See Section 4.2.2 for details.

4.2.1 Regularization hyperparameter

The hyperparameter of LASSO can be optimized in multiple ways, each one of them with different merits and disadvantages. A first approach is to optimize once and then keep it fixed for the whole test period. Although it requires very low computation costs, the limitation of this approach is that it assumes that the hyperparameter does not change over time. This assumption might hinder the performance of the estimator as the regularization parameter does not change even when the market might do.

A second approach is to recalibrate the hyperparameter on a periodic basis using a validation dataset. Although this method yields good results, tuning the recalibration frequency and calibration window is complicated, the computational cost is large, and the results may vary between datasets [58].

A third option is to recalibrate the hyperparameter periodically, but using cross-validation (CV): splitting the data into disjoint partitions, using each possible partition once as a test dataset with the remaining data as the training dataset, and selecting the hyperparameter that performs the best across all partitions [109]. Although this approach is highly accurate, its computation costs are very large.

A fourth option is to periodically update the hyperparameter but using information criteria, e.g. the Akaike information criterion (AIC) or the Bayesian information criterion [57, 110, 69]. As before, this involves training multiple LASSO models to compute the information criteria for each possible hyperparameter value, which in turn leads to a high computational cost.

Lastly, one can use the least angle regression (LARS) LASSO [111] for estimating the model instead of the coordinate descent implementation. This estimation procedure has the advantage of computing the whole LASSO solution path, which in turn allows to compute the information criteria or perform CV much faster.

4.2.2 Selecting the regularization hyperparameter

To select we propose a hybrid approach. On a daily basis, we estimate the hyperparameter using the LARS method with the in-sample AIC. Then, using the optimal obtained from the LARS method, we recalibrate the LEAR using the traditional coordinate descent implementation.

The reason for proposing this hybrid approach is that it provides a good trade-off between computational complexity and accuracy. In particular, it leverages the computational efficiency of LARS for ex-ante selection with the predictive performance on short calibration windows of the coordinate descent LASSO.

It is important to note that we have studied multiple approaches to select : (i) daily recalibration, CV, with coordinate descent; (ii) daily recalibration, CV, with LARS; (iii) daily recalibration with LARS and AIC. However, the computational cost of the first method was too high (in the same order of magnitude as the cost of the DNN model), and the accuracy of the other two was not good. By contrast, the proposed approach had a performance on par with coordinate descent LASSO using CV, but with a computational cost that was an order of magnitude lower.

4.3 The DNN model

The second model is the DNN [59], one of the most simple DL models whose input features and hyperparameters can be optimized and tailored for each case study without the need of expert knowledge.

4.3.1 Structure

The DNN is a deep feedforward neural network that contains 4 layers, employs the multivariate framework (single model with 24 outputs), is estimated using Adam, and its hyperparameters and input features are optimized using the tree Parzen estimator [108], i.e. a Bayesian optimization algorithm. The DNN model is visualized in Figure 4.

4.3.2 Training dataset

For estimating the hyperparameters, the training dataset is fixed and comprises the four years prior to the testing period. For evaluating the testing dataset, the DNN is recalibrated on a daily basis using a calibration window of four years.

In all cases, the training dataset is split into a training and a validation dataset, with the latter being used for two purposes: performing early stopping [112] to avoid overfitting and optimizing hyperparameters/features. While the validation dataset alwawys comprises 42 weeks, the split between the training and validation datasets depends on whether the validation dataset is used for hyperparameter/feature selection or for the recalibration step:

-

1.

For estimating the hyperparameters, as the validation dataset is used to guide the optimization process, the validation dataset is selected as the last 42 weeks of the training dataset. This is done to keep the training and validation datasets completely independent and to avoid overfitting101010Similar as it is done when splitting the dataset between the training and test dataset..

-

2.

For the testing phase, as the validation dataset is only used for early stopping, it is defined by randomly selecting 42 weeks out of the total 208 weeks employed for training. This is done to ensure that the dataset used for optimizing the DNN parameters includes up-to-date data111111For hyperparameter optimization, as the validation dataset represents the most recent weeks of data, the neural network is trained with data that is almost one year old. While this is not a big problem when decididing on the DNN structure, it should be avoided during testing to ensure that the DNN captures new market effects..

As example, let us consider the training and evaluation of a DNN in the Nord Pool market. Before evaluating the DNN, the hyperparameter and features of the DNN are optimised. For that, the employed dataset comprises the data between 01.01.2013 and 26.12.2016, of which the training dataset represents the first 166 weeks, i.e. 01.01.2013 to 07.03.2016, and the validation dataset the last 42, i.e. 08.03.2016 to 26.12.2016. During the evaluation of the model, i.e. after the hyperparameter and feature selection, the training and validation datasets comprise the last four years of data but are randomly suffled. For example, to evaluate the DNN during 15.02.2017, the training and validation datasets would represent the data between 20.02.2013 and 14.02.2017, of which 166 randomly selected weeks would define the training dataset and the remaining 42 the validation dataset.

4.3.3 Hyperparameter and feature selection

As in the original DNN paper [59], the hyperparameters and input features are optimized together using the tree-structured Parzen estimator [108], a Bayesian optimization algorithm based on sequential model-based optimization. To do so, the features are modeled as hyperparameters, with each hyperparameter representing a binary variable that selects whether or not a specific feature is included in the model (as explained in [43]). In more detail, to select which of the 241 available input features are relevant, the method employs 11 decision variables, i.e. 11 hyperparameters:

-

1.

Four binary hyperparameters (1-4) that indicate whether or not to include the historical day ahead prices , , , . The selection is done per day121212This is done for the sake of simplicity to speed up the optimization procedure of the feature selection. In particular, an alternative could be to use a binary hyperparameter for each individual historical prices; however, is most markets, that would mean using 24 as many hyperparameters as there are 24 different prices per day., e.g. the algorithm either selects all the prices of days ago or it cannot select any price from day , hence the four hyperparameters.

-

2.

Two binary hyperparameters (5-6) that indicate whether or not to include each of the day-ahead forecasts and . As with the past prices, this is done for the whole day, i.e. a hyperparameter either selects all the elements in or none.

-

3.

Four binary hyperparameters (7-10) that indicate whether or not to include the historical day-ahead forecasts , , , and . This selection is also done per day.

-

4.

One binary hyperparameter (11) that indicates whether or not to include the variable representing the day of the week.

In short, 10 binary hyperparameters indicating whether or not to include 24 inputs each and another binary hyperparameter indicating whether or not to include a dummy variable.

Besides selecting the features, the algorithm also optimizes eight additional hyperparameters: 1) the number of neurons per layer, 2) the activation function, 3) the dropout rate, 4) the learning rate, 5) whether or not to use batch normalization, 6) the type of data preprocessing technique, 7) the initialization of the DNN weights, and 8) the coefficient for L1 regularization that is applied to each layer’s kernel.

Unlike the weights of the DNN that are recalibrated on a daily basis, the hyperparameter and features are optimized only once using the four years of data prior to the testing period. It is important to note that the algorithm runs for a number of iterations, where at every iteration the algorithm infers a potential optimal subset of hyperparameters/features and evaluates this subset in the validation dataset. For the proposed open-access benchmark models, is selected as 1500 iterations to obtain a trade-off between accuracy and computational requirements131313It can be empirically observed that the performance of the models barely improves after 1000 iterations. Moreover, performing 1500 iteration takes approximately just one day on a regular quadcore laptop like the i7-6920HQ, a computation cost very acceptable when the algorithm has to run only once..

4.4 Ensembles

For the open-access benchmark, in order to have benchmark predictions when evaluating ensemble techniques, we also proposose ensembles of LEAR and DNNs as open-access benchmarks of ensembles methods. For the LEAR, the ensemble is built as the arithmetic average of forecasts across four calibration window lengths: 8 weeks, 12 weeks, 3 years, and 4 years. For the DNN, the ensemble is built as the arithmetic average of four different DNNs that are estimated by running the hyperparameter/feature selection procedure four times. In particular, the hyperparameter optimization is asymptotically deterministic, i.e. the global optimum is found for an infinite number of iterations. However, for a finite number of iterations and using a different initial random seed, the algorithm is non-deterministic and every run provides a different set of hyperparameters and features. Although each of these hyperparameter/feature subsets represent a local minimum, it is impossible to establish which of the subsets is better as their relative performance on the validation dataset is nearly identical. This effect can be explained due to the DNN being a very flexible model and thus different network architectures being able to obtain equally good results.

4.5 Software implementation

The proposed open-access models are developed in python: the LEAR is implemented using the scikit-learn library [113] and the DNN model using the Keras library [114]. The reason for selecting python is that it is one of the most widely used programming languages, especially in the context of ML and statistical inference.

5 Guidelines and best practices in EPF

As motivated in the introduction, the field of EPF suffers from several problems that prevent having reproducible research and establishing strong conclusions on what methods work best. In this section, we outline some of these issues and provide some guidelines on how to address them.

5.1 Length of the test period

A common practice in EPF is to evaluate new methods on very short test periods. The typical approach is to evaluate the method on 4 weeks of data [26, 95, 18, 19, 51, 41, 42, 93, 99, 49, 91, 92, 96, 22, 24, 25, 94, 30, 29, 87], with each week representing one of the four seasons in the year. This is problematic for three reasons:

-

1.

Selecting four weeks can lead to cherry-picking the weeks where a given method excels, e.g. a method that performs bad with spikes could be evaluated in a week with fewer spikes, leading in turn to biased estimations of the forecasting accuracy. While this is an ethical issue that most researchers would avoid, establishing four weeks testing periods as the standard does facilitate the malpractice and it should be avoided.

-

2.

Assuming that the four weeks are randomly selected and no bias is introduced in the selection, it is still not possible to guarantee that these four weeks are representative of the price behavior on a whole year. Particularly, even within a given season, the price dynamics can change dramatically, e.g. during winter there are weeks with a lot of sun and wind but there are also weeks without them. Therefore, picking only a week per season rarely represents the average performance of a forecaster in a give dataset.

-

3.

There are situations in the electrical grid that do not occur very often but that can have a very large effect on electricity prices, e.g. when several power plants are under maintenance at the same time. Forecasting methods need to be evaluated under those conditions to ensure that they are also accurate under extreme events. By selecting four weeks most of these effects are neglected.

To avoid this problem, we recommend using a minimum of one year as a testing period. This ensures that forecasting methods are evaluated considering the complete set of effects that take place during the year. To guarantee that all researchers have access to this type of data, the open-access benchmark dataset that we propose contains data from several markets and employs a testing period of two years. In addition, the open-access benchmark can be directly accessed using the proposed epftoolbox library [60, 61].

5.2 Benchmark models

A second issue with many EPF publications is that new methods are not compared with well-established methods [42, 21, 48, 49, 34, 25, 50, 90, 27, 95, 18, 19, 100, 20, 93, 16, 14, 23, 46, 78, 36] or resort to comparisons using either outdated methodologies or simplified methods [26, 51, 52, 22, 41, 24, 91, 92, 44, 13, 29, 30, 28, 45, 15, 47, 85, 86, 37].

This poses a problem since it becomes very hard to establish which algorithms work best and which ones do not. To address this issue, we recommend using well-established state-of-the-art open-source methods and a common benchmark dataset. With that in mind, we have provided and make freely available an open-access benchmark dataset comprising 5 markets (as described in Section 3), and we have implemented, thoroughly tested, and made freely available two state-of-the-art forecasting methods (as described in Section 4) and their day-ahead predictions for all 5 datasets over a period of two years (as described in Section 6). Additionally, we have implemented all these resources in an easy-to-use toolbox [60] and built an adequate documentation [61].

5.3 Open-access

A third issue in the field of EPF is that datasets are usually not made publicly available and the code of the proposed methods is not shared. This poses four obvious problems:

-

1.

Research cannot be reproduced as data is not available. This goes against one of the main principles of science as all research should be reproducible.

-

2.

The progress of EPF research is hindered since it is hard to establish which methodologies work well. Consequently, researchers spend unnecessary time re-evaluating methodologies that have been evaluated already.

-

3.

Comparing new methods with published ones becomes very challenging because researchers have to re-implement methods from the literature. As a result, comparisons with state-of-the-art methods are often avoided, and new methods are usually compared with simple and easy-to-implement methods.

-

4.

When new methods are proposed, they cannot be compared with published methods under the same circumstances. This leads to comparisons under different conditions and opens up the door to wrong implementations of the original methods, which in turn leads to results that are not correct.

As these problems are critical, we directly try to address them by providing an open-access benchmark/toolbox comprising five datasets, two state-of-the-art methods, and a set of day-ahead forecasts of the latter two methods. In addition, we encourage researchers in EPF to share the developed codes and to either share their datasets or use an open-access benchmark dataset.

5.4 Evaluation metrics for point forecasts

In the field of EPF, the most widely used metrics to measure the accuracy of point forecasts are the mean absolute error (MAE), the root mean square error (RMSE), and the mean absolute percentage error (MAPE):

| (4) | ||||

| (5) | ||||

| (6) |

where and respectively represent the real and forecasted price on day and hour , and is the number of days in the out-of-sample test period, i.e. in the test dataset.

Since absolute errors are hard to compare between different datasets, the MAE and RMSE are not always very informative. Moreover, since electricity costs and profits are often linearly dependent on the electricity prices, metrics based on quadratic errors, e.g. RMSE, are hard to interpret and do not accurately represent the underlying problem of most forecasting users. In particular, in most electricity trade applications, the underlying risk, profits, and costs depend linearly on the price and on the forecasting errors. Hence, linear metrics represent better than quadratic metrics the underlying risks of forecasting errors.

Similarly, since MAPE values become very large with prices close to zero (regardless of the actual absolute errors), the MAPE is usually dominated by the periods of low prices and is also not very informative. While the symmetric mean absolute percentage error (sMAPE) defined141414Note, that there are multiple versions of sMAPE, here we consider the most sensible one according to [115]. as:

| (7) |

solves some of these issues, it has (as any metric based on percentage errors) a statistical distribution with undefined mean and infinite variance [116].

5.4.1 Scaled errors

In this context, several studies advocate for the use of scaled errors [5, 116, 117], where a scaled error is simply the MAE scaled by the in-sample MAE of a naive forecast. A scaled error has the nice interpretation of being lower/larger than one if it is better/worse than the average naive forecast evaluated in-sample.

A metric based on this concept is the mean absolute scaled error (MASE), and in the context of one-step ahead forecasting is defined as [116]:

| (8) |

where is the price in the in-sample, i.e. training, dataset (note that in EPF ), is the one-step ahead naive forecast of , i.e. , is the number of out-of-sample (test) datapoints, and the number of in-sample (training) datapoints. For seasonal time series, the MASE may be defined using the MAE of a seasonal naive model in the denominator [5, 117].

5.4.2 Relative measures

While scaled errors do indeed solve the issues of more traditional metrics, they have other associated problems that make them unsuitable in the context of EPF:

-

1.

As MASE depends on the in-sample dataset, forecasting methods with different calibration windows will naturally have to consider different in-sample datasets. As a result, the MASE of each model will be based on a different scaling factor and comparisons between models cannot be drawn.

-

2.

The same argument applies to models with and without rolling windows. The latter will use a different in-sample dataset at every time point while the former will keep the in-sample dataset constant.

-

3.

In ensembles of models with different calibration windows, the MASE cannot be defined as the calibration window of the ensemble is undefined.

-

4.

Drawing comparisons across different time series is problematic as electricity prices are not stationary. For example, an in-sample dataset with spikes and an out-of-sample dataset without spikes will lead to a smaller MASE than if we consider the same market but with the in-sample/out-sample datasets reversed.

To solve these issues, we argue that a better metric is the relative MAE (rMAE) [116]. Similar to MASE, rMAE normalizes the MAE by the MAE of a naive forecast. However, instead of considering the in-sample dataset, the naive forecast is built based on the out-of-sample dataset. In the context of EPF, rMAE is defined as:

| (9) |

where the factor cancels out in the numerator and the denominator. There are three natural choices for the naive forecasts:

-

1.

,

-

2.

,

-

3.

In the context of EPF, rMAE using is arguably the best choice for two reasons: (i) it is easier to compute than the one based on and, unlike the rMAE based on , it captures weekly effects; (ii) given a set of forecasting models, the relative ranking of the accuracy of the models is independent from the naive benchmark used (see last paragraph of this subsection for an explanation). Hence, for the remainder of the article we will use rMAE to explicitly refer to the rMAE based on . It is important to note that, similar to rMAE, one could also define the relative RMSE (rRMSE) by dividing the RMSE of each forecast by the RMSE of a naive forecast.

Since the dependence on the in-sample dataset is removed, using a rolling window is no longer a problem as the out-of-sample dataset stays the same. Similarly, models with different calibration windows can be compared and the rMAE of ensembles is properly defined. Moreover, as the metric is normalized by the MAE of a naive forecast for the same sample, the problem with drawing conclusions in non-stationary time series is mitigated. As before, we can also define the rMAE for seasonal time series:

Due to its better properties, rMAE should always be used to evaluate new methods in EPF. In particular, while it can be used in conjunction with other metrics, it is important to include and employ rMAE to obtain more fair evaluations and comparisons.

With that in mind, the accuracy of the open-access models in the open-access benchmark dataset is computed considering rMAE, sMAPE, MAPE, MAE, and RMSE. Then, an analysis of the different metrics is provided (see Section 6.4.2). Finally, the forecasts themselves are provided as csv files so that the accuracy results can be updated in case more adequate metrics are developed in the future.

As a final remark, let us to note that, given a set of forecasting models, the relative ranking of the accuracy of the models is independent from the naive benchmark used for the rMAE or MASE. Changing it simply changes the denominator but preserves the numerator, and since the change in the denominator is the same across all methods, the relative ranking is preserved. Furthermore, as the numerator is the MAE, it follows that the ranking based on the rMAE or MASE will be the same as that based on the MAE.

5.5 Statistical testing

While using adequate metrics to compare the accuracy of the forecasts is important, it is also necessary to analyze whether any difference in accuracy is statistically significant. This is paramount to conclude whether the difference in accuracy does really exist and is not simply due to random differences between the forecasts. Despite its importance, the use of statistical testing has been downplayed in the EPF literature [5]. In particular, most publications only compare the accuracy in terms of an error metric and do not analyze the statistical significance of the accuracy differences. This trend needs to be corrected in order to compare forecasting approaches with statistical rigor. Particularly, new studies need to ensure that:

-

1.

Any new method is compared against well-established methods using a statistical test.

-

2.

The forecasts of the proposed methods are provided as open-access datasets. This ensures that, when new models are proposed, the difference in accuracy with the published methods can be analyzed in terms of statistical testing.

To facilitate statistical testing, we include in the propose open-source epftoolbox library [60, 61] the two most widely used statistical tests in EPF, i.e. the Diebold-Mariano and the Giacomini-White tests.

5.5.1 The Diebold-Mariano test

The Diebold-Mariano (DM) test [118] is probably the most commonly used tool to evaluate the significance of differences in forecasting accuracy. It is an asymptotic z-test of the hypothesis that the mean of the loss differential series:

| (10) |

is zero, where is the prediction error of model Z for day and hour , and is the loss function. For point forecasts, we usually take with or , which corresponds to the absolute and squared losses, respectively; for probabilistic forecasts, may be any strictly proper scoring rule, in particular the pinball loss, the continuous ranked probability score (CRPS), or the energy score [6, 65, 66]. Given the loss differential series, we compute the statistic:

| (11) |

where and are the sample mean and standard deviation of , respectively, and is the length of the out-of-sample test period. Under the assumption of covariance stationarity of , the DM statistic is asymptotically standard normal, and one- or two-sided asymptotic tail probabilities can be easily computed.

It is important to note three things. Firstly, the DM test is model-free, i.e. it compares forecasts (of models), not models themselves. Secondly, although in the standard formulation [118] the DM test compares forecasts via the null hypothesis of the expected loss differential being zero, it is more informative to compute the -values of two one-sided tests:

-

1.

with the null hypothesis ,

-

2.

with the alternative hypothesis null .

The lower the -value151515Recall, that the -value is the probability of obtaining results (in our case – loss differentials) at least as large as the ones actually observed, assuming that the null hypothesis is correct., i.e. the closer it is to zero, the more the observed data is inconsistent with the null hypohtesis. If the -value is less than the commonly accepted level of 5%, the null hypothesis is typically rejected. In the DM test, this means that the forecasts of model B are significantly more accurate than those of model A.

Thirdly, the DM test requires (only) that the loss differential be covariance stationary.161616Actually covariance stationarity is sufficient but may not be strictly necessary [119]. This may not be satisfied by forecasts in day-ahead markets, since the predictions for all 24 hours of the next day are computed at the same time, using the same information set. Hence, following [65], we recommend two variants of the DM test in the context of day-ahead EPF:

-

1.

a univariate variant with 24 independent tests performed171717We assume that a day-ahead market has 24 prices. For markets with prices every half hour, the univariate variant comprises 48 independent tests., one for each hour of the day, and comparisons based on the number of hours for which the predictions of one model are significantly better than those of another, i.e. the number of hours for which the null hypothesis is rejected,

-

2.

a multivariate variant with the test performed jointly for all hours using the ‘daily’ or multivariate loss differential series:

(12) where is the 24-dimensional vector of prediction errors of model Z for day , is the -th norm of that vector with or .

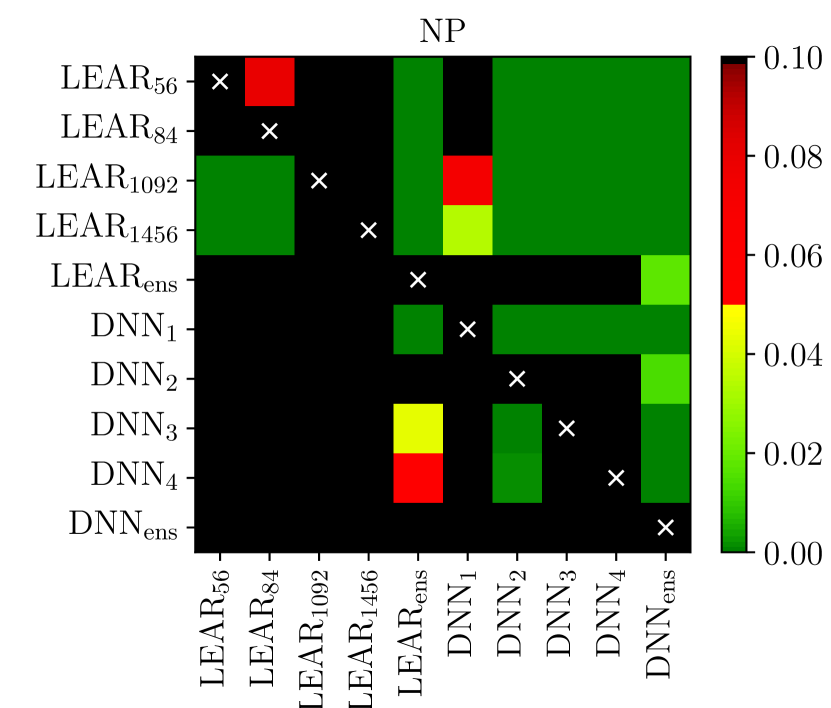

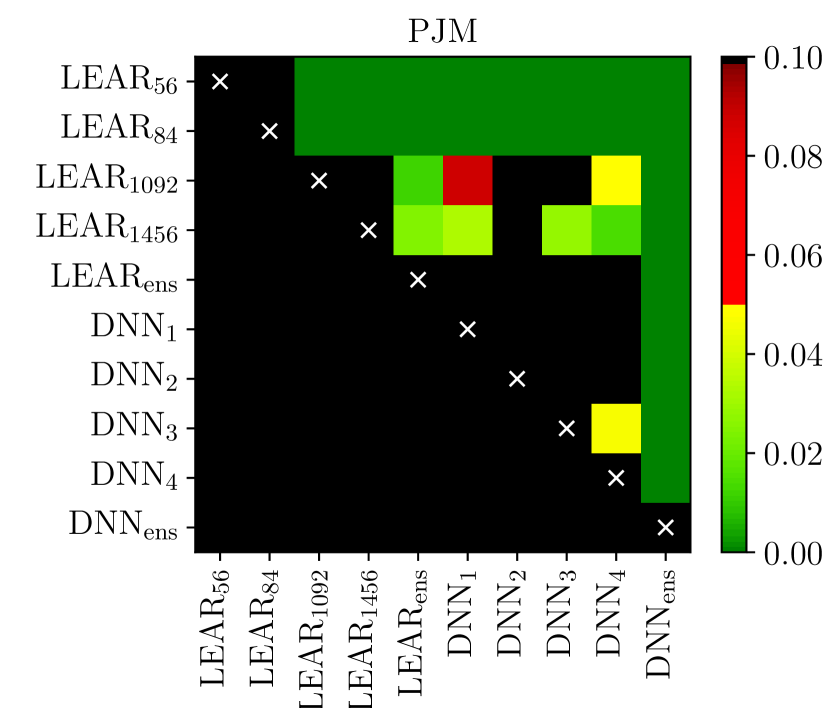

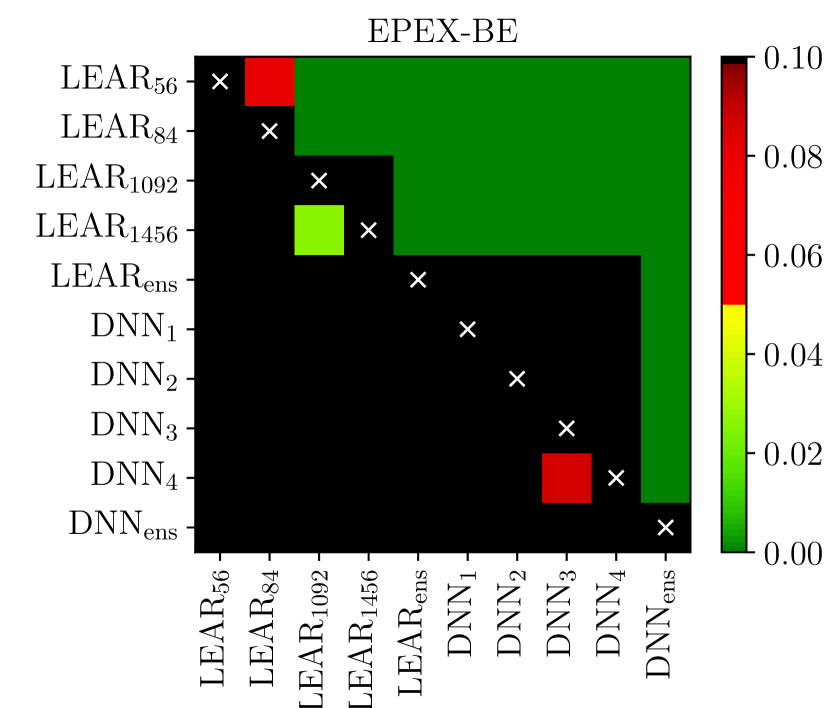

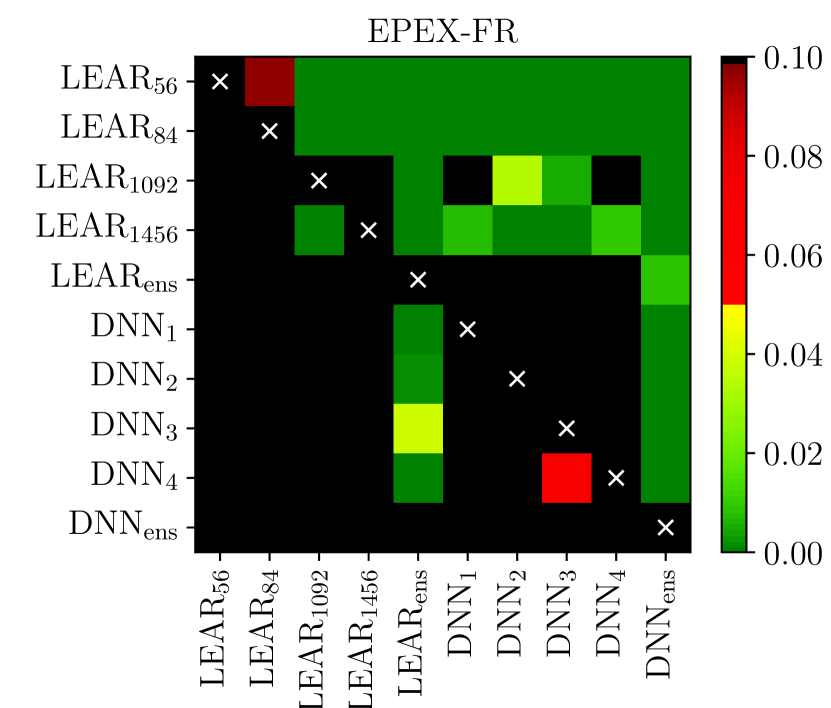

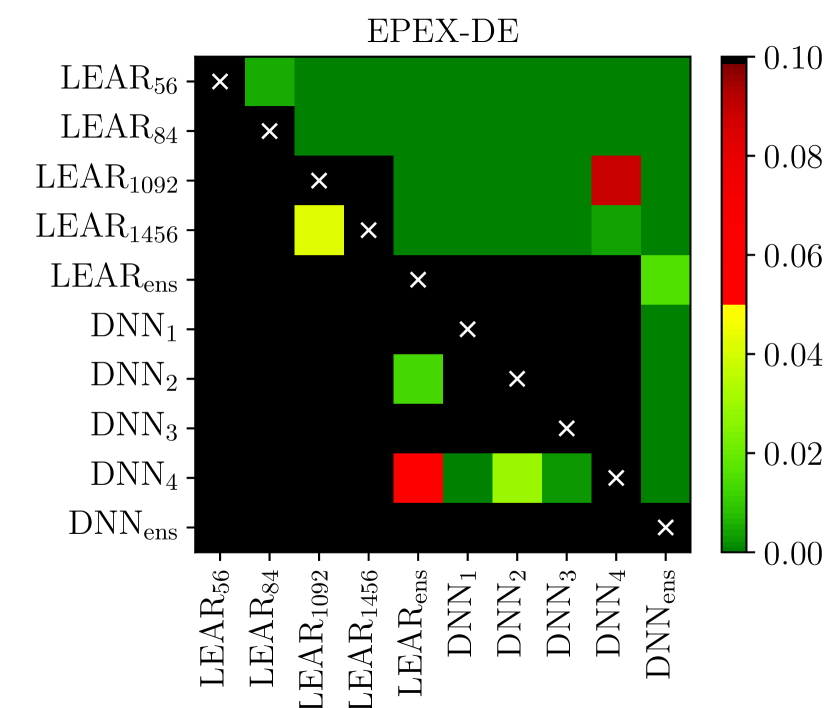

The univariate version of the test has the advantage of providing a deeper analysis as it indicates which forecast is significantly better for which hour of the day [120, 121, 55, 59, 6, 66]. The multivariate version, introduced in [57], enables a better representation of the results as it summarizes the comparison in a single -value, which can be conveniently visualized using heat maps arranged as chessboards [9, 58, 76, 10], see Figure 5.

5.5.2 The Giacomini-White test

In some of the more recent EPF studies [77, 122, 123], the DM test has been replaced by the Giacomini-White (GW) test [124] for conditional predictive ability. The latter is preferred because it can be regarded as a generalization of the DM test for unconditional predictive ability: while both tests can be used for nested and non-nested models181818This holds as long as the calibration window does not grow with the sample size [125]. This is satisfied for rolling windows, but not for extended calibration windows., only the GW test accounts for parameter estimation uncertainty through ‘conditioning’ [65].

Like the DM test, also the GW test has two variants in day-ahead EPF – the univariate and the multivariate. Without loss of generality, let us focus on the latter. It starts by building a multivariate loss differential series, see (12), for a pair of forecasts (of models A and B). Next, the test considers the following regression:

| (13) |

where contains elements from the information set on day , i.e. a constant and lags of . Note that , i.e. is not the 24-dimensional vector of prediction errors for day and model but simply an error term in the regression. Also note that using this notation the DM test can be written as [125]:

| (14) |

i.e. with containing just a constant. Finally, like for the DM test, to check the significance of differences in forecasting accuracy, the -values of two one-sided tests can be computed. The interpretation and possible visualization (see Figure 5) are analogous to that of the DM test.

5.6 Recalibration

An issue with many EPF studies is that forecasting models are not recalibrated. Instead, they are often estimated once using the training dataset and directly evaluated in the whole test dataset. This is problematic as it does not represent real-life conditions where forecasting models are retrained (often on a daily basis) to account for the latest market information.

To have models that are evaluated in realistic conditions, they need to be retrained considering the new incoming flow of market information. As an example, for the day-ahead market, a forecasting model should be retrained on a daily basis as new information is available. Considering a testing period of a year, this means that a realistic evaluation requires estimating the forecasting model 365 times.

5.7 Ex-ante hyperparameter optimization

A common issue in the current EPF literature is that the hyperparameter selection is often either done ex-post [51, 126, 127, 128, 129, 49] or its details are not sufficiently explained [13, 82, 79, 21, 93, 99, 48, 91, 92, 96, 37]. As an example, when models based on neural networks are proposed, the details on how the number of neurons are selected are usually not provided. In other cases, while the approach is provided, it is often based on analyzing different configurations of neurons using the test dataset and selecting the one that works best, i.e. ex-post hyperparameter selection.

Not providing enough details on how hyperparameters are selected is an obvious problem as it prevents reproducing research. Similarly, performing hyperparameter optimization ex-post leads to overfitting the test dataset, i.e. the model is partially optimized using the same dataset used for evaluating the model, and it grants the model an unfair and non-existent advantage over other models.

To prevent this, the selection of hyperparameters should be explicitly explained and always performed ex-ante using a validation dataset. With that motivation, for the open-access methods proposed, not only do we explain how the hyperparameters are obtained, but we also provide within the toolbox [60, 61] a module for hyperparameter selection and the files containing the results of the hyperparameter optimization of the current study.

5.8 Computation time

An even more common problem is the fact that new models are very rarely compared in terms of their computational requirements [51, 41, 42, 91, 92, 96, 94, 32, 97, 95, 19, 100, 24, 20, 90, 22, 37]. Although a model might be marginally better than another, it might not be worthwhile to deploy it in a practical application if its computational requirements are much larger. Particularly, higher computational requirements might pose two problems:

-

1.

As mentioned before, forecasting models should ideally be recalibrated on a daily basis. Hence, a forecasting method is only suitable if its computational time allows this recalibration to take place. In this context, the maximum available time for estimating a model will depend on each electricity market but, as a rule of thumb, it can be argued that any model that requires more than 30 min or 1 h will unlikely be suitable for forecasting prices in the spot markets.

-

2.

Besides recalibration, the second issue with computation time is its cost. If the computational capabilities are too large, the benefits of using a marginally better forecast might be lower than the cost of running the forecasting model on a much more expensive computer.

Hence, when new forecasting models are proposed, we argue that it is very important to provide their computation times. Moreover, we also argue that for a model to be better than the existing methods, it does not necessarily have to be the most accurate one. Instead:

-

1.

If its computational time is large, i.e. in the order of minutes, the model should indeed be more accurate than all state-of-the-art models, e.g. DNNs.

-

2.

If its computational time is small, i.e. in the order of seconds, the model should be more accurate than the state-of-the-art models with low computational requirements, e.g. LEAR.

In this article, we provide an analysis of the computational requirements of the proposed open-access models so other researchers can easily make such comparisons.

5.9 Reproducibility

Another related issue is that some studies lack enough details to replicate the research. Missing details vary from study to study but the four most common are:

-

1.

the dataset used for testing and evaluation is not defined [31, 32, 33, 34, 35, 36, 37];

-

2.

the dataset used for training is not defined [41, 42, 21, 33, 35];

-

3.

the inputs of the model are unclear [38, 35, 39, 40, 36];

-

4.

the selection of hyperparameters is unclear [13, 82, 79, 21, 93, 99, 48, 91, 92, 96, 37].

To correct this, future EPF papers should provide enough details to allow replication and reviewers should verify that all necessary details of the employed datasets are always provided.

5.10 Data contamination

Another recurrent issue in the EPF literature is data contamination, which appears when part of the training dataset is used for testing. Particularly, when working with time series data the test dataset should always comprise the last part of the dataset to avoid data contamination. If this is not done, the models can overfit the testing dataset and their accuracy can be overestimated.

Despite the importance of correctly separating the training/validation dataset from the testing dataset, some studies in EPF:

-

1.